Evidence suggests that digital public infrastructure (DPI) can greatly simplify tax administration and boost tax compliance. However, some persistent challenges must first be addressed, including poor access to data.

Digital public infrastructure (DPI) could become a game changer for the digitalization of governments and societies. The DPI concept builds on open-source, interoperable and scalable pillars – akin to Lego blocks. These can be assembled and combined to create inclusive, resilient, and adaptable digital solutions that improve public services and, in turn, drive economic development.

Two such pillars – the digital ID system (DIS) and digital merchant payments (DMPs) – hold great potential to strengthen increasingly digitalized tax administrations. This potential is even bigger in resource-strapped African countries, where tax agencies are prioritizing and investing in digital transformations.

For example, it is believed that a DIS can help tax authorities unambiguously identify, verify and track taxpayers over time and, at the same time, make registration and compliance easier for taxpayers. Likewise, DMPs could potentially create a digital ‘paper trail’ which is crucial for a tax authority to accurately identify taxable income and enforce compliance.

Based on our analysis of evidence from several countries, for African governments to transform such potential into meaningful impact, wider administrative, institutional and political factors need to be considered. To reap the tax benefits of DPI, governments need to consider adoption patterns, establish seamless data-exchange systems (a third pillar of DPI), and ensure their tax administration has the tools and capacity to use this data appropriately.

Importantly, and beyond tax administration, our analysis of evidence suggests that DPI offers huge whole-of-government opportunities for African countries.

Digital public infrastructure shows global promise

While DIS and DMP technologies are not yet fully widespread, they have shown promise in several countries. For instance:

- India’s successful DPI implementation, integrated with tax administration systems, has improved taxation outcomes and reduced fraud.

- South Korea’s active encouragement of DMP adoption has led to improved tracking and simplified tax filing, increasing compliance.

- Similar success stories come from China and the USA, where third-party reporting on electronic sales data has significantly increased compliance.

African experiences with digital public infrastructure

As with other technological improvements, policies promoting DISs and DMPs have also reached the African continent:

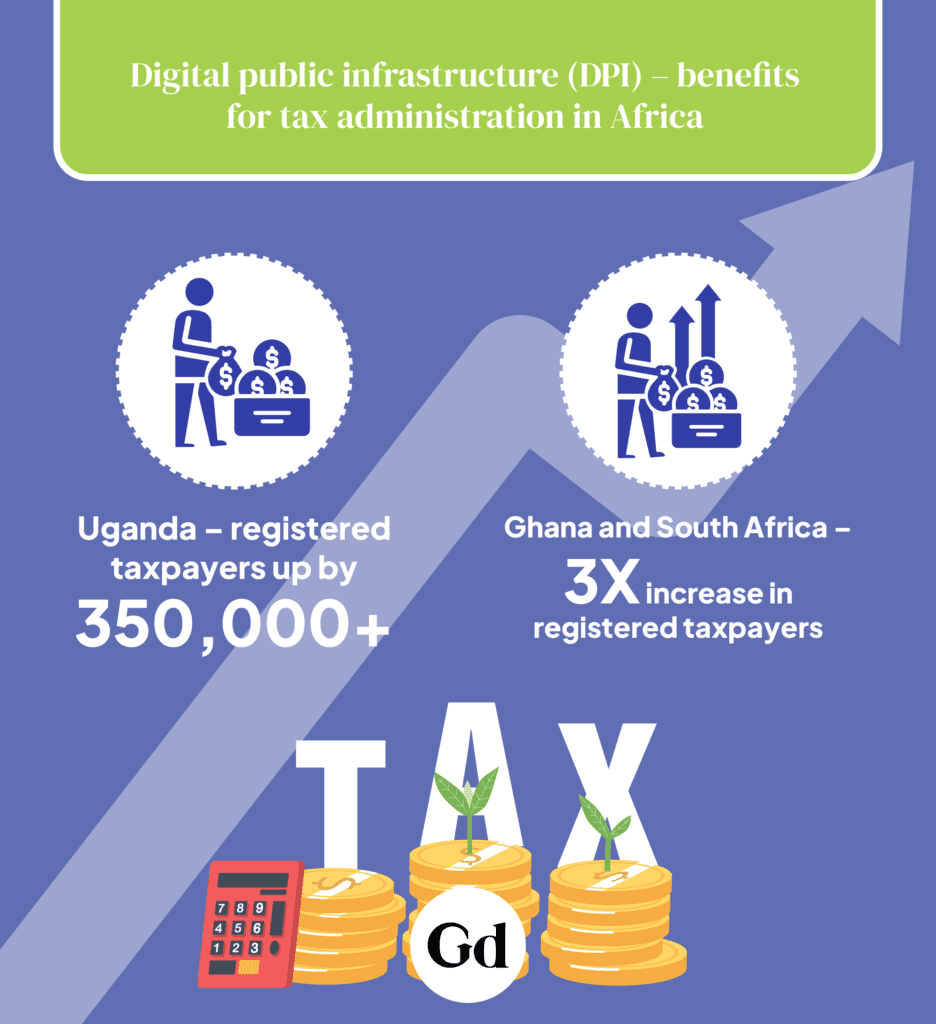

- The Uganda Revenue Authority integrated its registration system with that of the National Identification and Registration Agency to facilitate an online registration process that connects national ID numbers and tax identification numbers. As a result, in 2022 more than 350,000 taxpayers, who were mainly informal, registered with the revenue authority. Moreover, qualitative insights suggest a high level of satisfaction with the service.

- Similarly, the Ghana Revenue Authority leveraged a DIS for tax registration by collaborating with the National Identification Authority, which seamlessly transferred identity information to the revenue authority. This move by the revenue authority led to a threefold increase in total tax registrations in 2021–2022.

- In South Africa, registration numbers increased threefold thanks to the integration with the business registry.

- In Ethiopia, taxpayer registration has been recently integrated with Fayda, the country’s national DIS.

In these examples, while the incorporation of a DIS significantly augmented the tax base, this did not automatically translate into an increase in tax collection, for several reasons:

- the limited adoption of DIS

- the type of data shared, not necessarily fitting tax administrations’ needs, and often outdated

- the still patchy and ad-hoc data-sharing agreements, which do not allow seamless data sharing across the whole of government

- policy targets often prioritizing high registration targets, with still limited capacity to enforce compliance on a dramatically larger taxpayer base.

Digital merchant payments in Africa

For DMPs, the evidence is rather mixed. While several governments have introduced incentives for adoption, results are highly inconsistent and context-specific. While tax rebates seem to have worked in Korea, Greece and Colombia, point-of-sale (credit/debit card payment), subsidies were ineffective in Uruguay. In India, the 2016 demonetization increased reliance on electronic payments, which in turn raised the amount of tax revenue collected. Discouraging the use of cash by taxing cash deposits, as in Mexico, can indeed reduce its use, but it also pushed people to hold cash outside of the banking sector.

In Africa, more positive evidence is emerging:

- In Ghana, when a mobile money levy, with an exemption for DMPs, was introduced, DMP users viewed the exemption positively and held more positive perceptions of the tax system and government.

- In Rwanda, telecommunications companies waived a 1% DMP fee in March 2020, boosting adoption by 20% while reducing the use of cash. As fees returned in September 2021, usage declined by 5% but was still higher than pre-waiver levels.

However, reluctance in adopting DMPs persists among businesses with limited trust of and familiarity with technology, as does trading with cash-reliant peers and consumers along the supply chain. In addition, adopting DMP only partially affects businesses’ tax compliance, and only for a short period after adoption – businesses simply offset their digital sales with more expenses, leading to a net-zero tax effect.

The full potential of DMPs to strengthen tax administration remains untapped. As with DIS, crucial barriers to widespread adoption exist, and governments need to find ways to prevent tax avoidance responses from those taxpayers who do adopt DMPs.

Also, when DMP data is shared with tax administrations, it is unclear if and how such data is used in a tax agency setting of limited analytical skills and resources.

More broadly, however, the sharing of DMP data is far from being achieved. Governments have faced limitations and legal constraints with accessing DMP data. For private DMP data, governance and confidentiality issues remain unresolved, in contrast with the open-source, multistakeholder and collaborative conceptualization of DPI.

The tax administration system as DPI

Huge opportunities remain for tax administrations to efficiently integrate with transparent, inclusive, and replicable DPI solutions. Tax administration systems themselves could function as DPI, enabling direct access and usage of tax data for a variety of purposes, such as accessing loan services or other government services.

More policy-oriented research is needed to document and explore such potential, diagnosing challenges with – and measuring impacts of – DPI in tax systems.