The importance of climate finance may be clear, but its definitions and scale are not. In the first of GlobalDev’s special series on climate finance, this blog explains the core concepts and debates to help you navigate this critical topic.

As the world grapples with the escalating impacts of climate change, the importance of raising enough financial resources to drive the transition to a low-carbon economy and build resilience in vulnerable communities has become very clear.

More recently, financing options to manage the already-occurring impacts of climate change, known as losses and damages, have moved to the centre of policy attention. But although the huge importance of adequate finance is clear, much remains to be done. If we are to mitigate the most devastating effects of climate change, and help communities adapt to its escalating impacts, we must increase the scale of the finance, improve its quality, and ensure greater clarity on definitions and accounting methodologies.

What is climate finance?

No official definition exists for climate finance. In a very broad sense, it refers to: “local, national or transnational financing—drawn from public, private and alternative sources of financing—that seeks to support mitigation and adaptation actions that will address climate change” (UNFCCC 2023). But interpretations differ. What kinds of sources are considered when counting the financial flows?

The United Nations Convention on Climate Change (UNFCCC) calls on Parties with more financial resources to assist those that are less endowed and more vulnerable. It introduces the principle of ‘common but differentiated responsibility and respective capabilities’. It hence recognizes that countries’ historical contributions and vulnerabilities to climate change vary to a great degree, as do the impacts of climate change.

In political negotiations, Parties thus refer to what we can call international climate finance. This is climate finance from industrialized countries (so-called Annex I countries under the UNFCCC) for developing countries (non-Annex I) and is triggered by public intervention. It represents a much narrower definition of climate finance that excludes, for example, private companies’ investments and climate investments made by developing countries themselves.

The Paris Agreement reaffirms the obligation of developed countries to provide ‘new and additional financial resources’. For the first time under the UNFCCC process, it also encourages voluntary contributions by non-Annex I countries, and calls for making financial flows (public and private) consistent with low-carbon and climate-resilient development under Article 2.1c. The Paris Agreement also calls for a balance between finance for adaptation and mitigation.

How much are we talking about?

Under the Paris Agreement, all Parties communicate their plans for mitigation (and partially adaptation) action in Nationally Determined Contributions (NDCs). These plans are to be updated every five years and increase in ambition. Based on all NDCs submitted in 2020, the climate finance needs of developing countries have been estimated at around USD 6 trillion until 2030, and despite significant gaps in assessing and counting adaptation needs. Other conservative estimates stand at USD 4.5 – 5 trillion annually. This is in stark contrast to what is currently provided. The Biennial Assessment of the UNFCCC Standing Committee on Finance estimates climate finance flows of USD 803 billion per year on average in 2019–2020. The Climate Policy Initiative estimates USD 653 billion for the same period.

In 2009, developed countries’ governments pledged at COP15 to mobilize USD 100 billion a year by 2020 from a wide variety of sources, instruments and channels. But in 2020, total mobilized international climate finance had only reached USD 83.3 billion. This figure includes public finance (USD 68.3 billion), private finance (USD 13.1 billion), and export credits (USD 1.9 billion).

This broken promise has diminished trust in industrialized countries’ pledges and the negotiation process. Some NGOs, such as Oxfam, criticize the fact that up to 70% of this finance is in the form of loans. They argue that, if only grant equivalents were to be counted, the self-reported numbers on provided public finance are far exaggerated and would be in the range of just USD 21–24.5 billion. Developed countries have the chance to redeem trust, however, through setting a new and higher goal, the so-called new collective quantified goal (NCQG) on climate finance by the end of 2024, a process that was decided at COP26 in Glasgow.

Dimensions of climate finance: sources, financial instruments and purpose

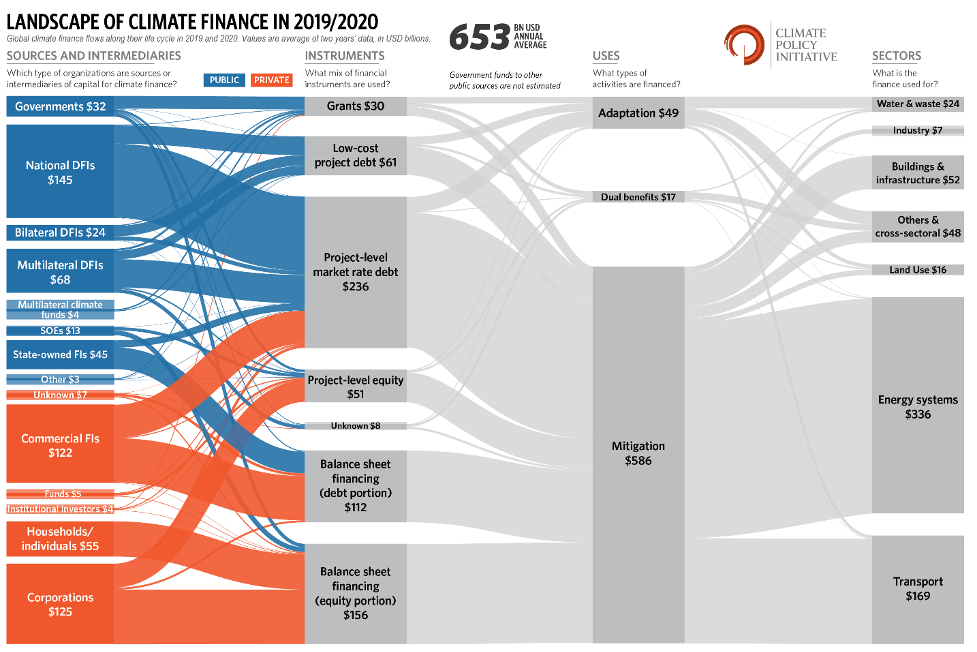

Since climate finance is so multifaceted, it is useful to break it down into different dimensions. The following numbers are based on the latest Climate Policy Initiative report (2022), which provides a comprehensive overview of global climate-related primary investments.

Figure 1: Landscape of climate finance in 2019/2020 (Source: Climate Policy Initiative, 2022)

The first dimension is the sources and intermediaries of climate finance, such as international vs. domestic sources, and public vs. private sources. In the years 2019 and 2020, 76% of all climate finance was raised and spent domestically (especially in the Global North and East Asia and Pacific). Although public actors have recently provided the most climate finance, the private sector nearly matches their investments.

The second dimension is the financial instruments used to distribute the funding, such as grants, loans, project-level equity, and balance sheet financing (both debt and equity portion). In 2019 and 2020, 61% of climate finance was issued as debt, 34% as equity, and only 5% as grants. Of these loans, only 16% were concessional (better than market conditions).

The third dimension is the type of activity financed – mitigation, adaptation, or both. In 2019 and 2020, 89.7% of finance went towards mitigation. Much of this came from private investors, as there are straightforward commercial benefits of mitigation that facilitate investment (e.g. in renewable energy).

Adaptation finance was estimated to be around USD 49 billion per year in 2019/2020 (7.5%) and thus remains severely underfunded. UNEP estimates annual adaptation needs at USD 160–340 billion by 2030 and USD 315–565 billion by 2050. Public actors provide most of the adaptation finance via multilateral and national development finance institutions. Tracking adaptation finance is less advanced than for mitigation, with substantial data gaps, especially from the private sector.

Finally, climate finance can be analyzed by the sectors that are targeted, which are mainly energy systems, transport, buildings and infrastructure, others and cross-sectoral, water and waste, land use, and industry (in descending order).

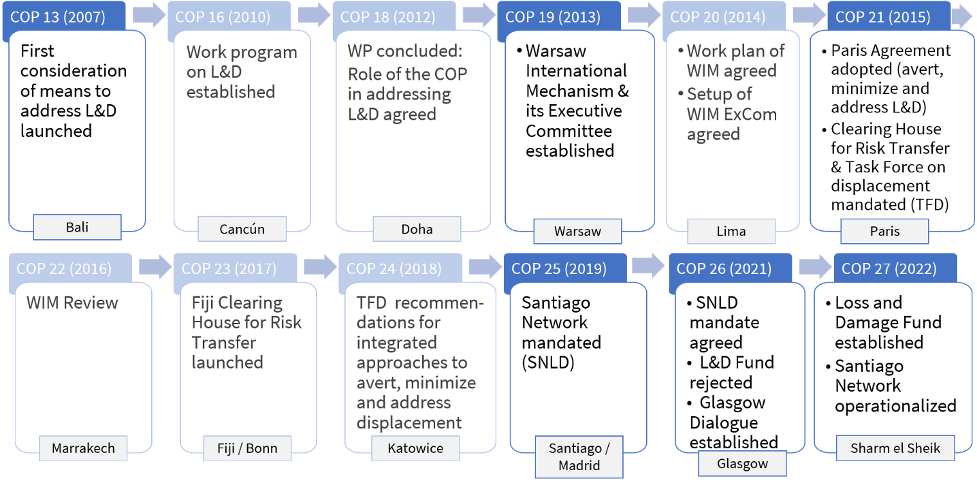

Finance for loss and damage – the next step for climate finance?

Agreeing to finance for loss and damage from the impacts of climate change—especially for addressing losses and damages once they have materialized—has long been a long and protracted process. But a breakthrough decision in 2022 at COP27 established ‘Loss and Damage Funding Arrangements and a Fund’. Details are to be elaborated by a Transitional Committee until COP28 in UAE this year.

Figure 2: Loss and damage under the UNFCCC (Source: Author, 2023)

Estimates of how much loss and damage finance is needed lie at USD 400 billion per year or between USD 290 and 580 billion by 2030. Civil society has called for a floor of USD 400 billion per year and an upward revision over time.

Until now, loss and damage has been addressed by other sources, such as humanitarian assistance, development assistance, climate funds (but not explicitly covered by their mandate), risk transfer, borrowing, and public finance. Some of this funding has been marked as adaptation finance or development assistance, but it has not been comprehensively tracked due to the absence of common definitions and methodologies. It remains to be seen if Loss and Damage Finance will be established as the ‘third pillar’ of climate finance, next to mitigation and adaptation.

Although the financial needs described here seem enormous, the absence of financial resources is not the problem. The issue is with the current focus of finances.

Fossil fuel subsidies of 51 major economies reached USD 6.8 trillion between 2011–2020 and skyrocketed to more than USD 1 trillion in 2022, the largest annual value ever recorded. This is around 40% more than total climate finance provided. Hence at the moment, the ‘net climate finance’ (i.e. the value of climate finance flows minus financial flows to high-emissions and maladaptive activities) is negative.

With a true shift towards net zero, many of the currently underfunded climate needs, including loss and damage, could be met.

This article is published as part of a series on climate finance organized in partnership with the United Nations University Institute for Environment and Human Security, the Munich Climate Insurance Initiative (MCII) and LUCCC/START.