Payday loan companies and other unscrupulous lenders exacerbate and perpetuate poverty. Understanding the key differences between “black” and “white” microfinance could help shape a future where financial inclusion truly leads to prosperity for all.

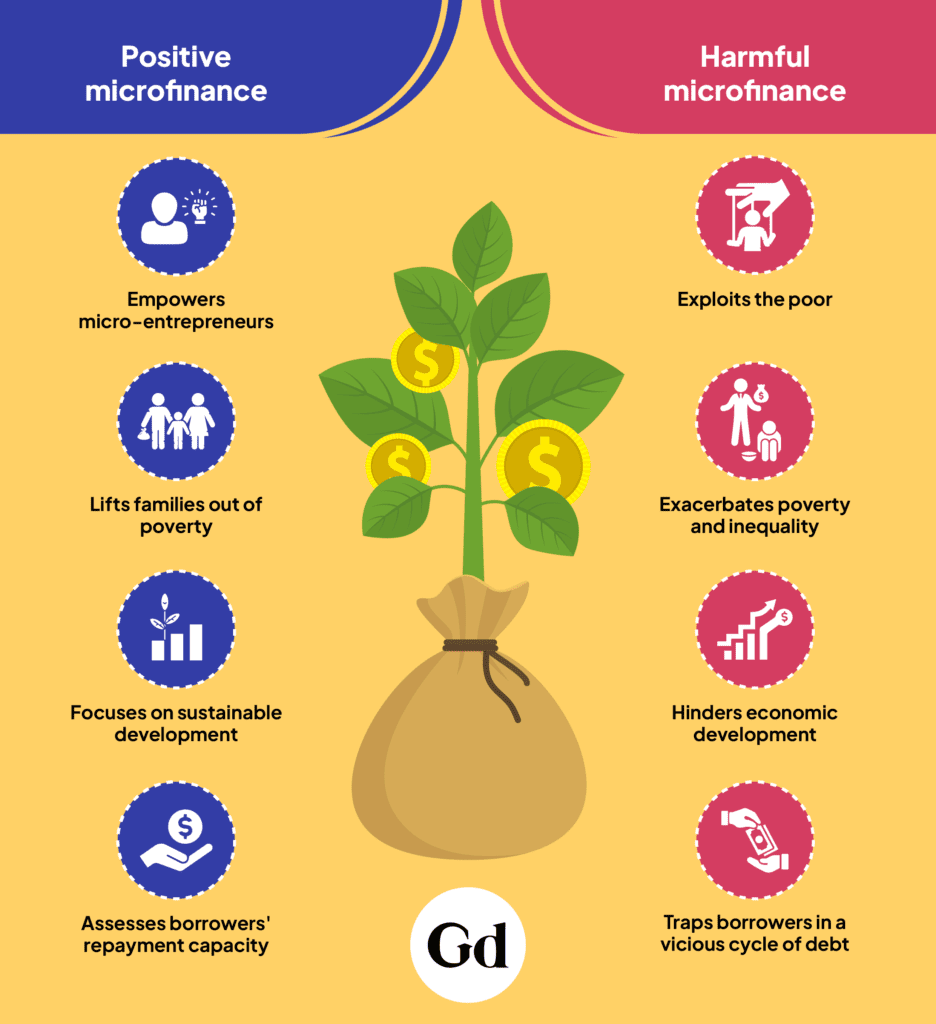

Microfinance has long been celebrated as a beacon of hope for impoverished communities worldwide, offering financial services to empower micro-entrepreneurs and lift families out of poverty. However, amidst the commendable efforts of genuine microfinance institutions lie so-called “black” microfinance, a shadowy and often overlooked realm.

“Black” microfinance embodies the exploitative lending practices that perpetuate cycles of poverty rather than breaking them. While genuine microfinance aims to provide real and impactful financial services to underserved populations engaged in micro-entrepreneurship or agribusiness, “black” microfinance operates under the guise of accessibility, offering seemingly convenient loans that ultimately burden borrowers with exorbitant interest rates and insurmountable debt.

Unlike its so-called “white” counterpart, which focuses on sustainable development and poverty alleviation, “black” microfinance adopts a model of lending that prioritizes profit over people through short-term, high-cost loans.

These programs offer quick and easy access to loans without adequately assessing borrowers’ repayment capacities. Nor do they provide financial education. As a result, borrowers find themselves trapped in a vicious cycle of debt, unable to escape the clutches of predatory lenders. Studies have shown that high-interest loans from payday lenders and “black” microfinance institutions lead to debt traps and worsen financial instability among the poor.

The consequences of “black” microfinance are dire. It exacerbates poverty and perpetuates socio-economic inequality. Families burdened by high-interest loans struggle to meet their basic needs, sacrificing their well-being and future prospects in a desperate attempt to repay debts that continue to mount. Moreover, the adverse effects extend beyond individual households and reverberate through entire communities, hindering efforts to improve economic development.

For example, payday loans, often characterized by exorbitant interest rates and aggressive collection practices, can trap borrowers in cycles of debt and make it difficult for them to escape poverty. Research highlights that borrowers of payday loans are more likely to face financial distress and have a higher risk of default, leading to severe economic and social consequences.

Further supporting this, the U.S. government’s Consumer Financial Protection Bureau (CFPB) reports that the costs associated with payday lending often outweigh the benefits, leading to prolonged financial hardship for borrowers.

Drawing parallels with loan sharks and other informal (unregulated) lending practices, “black” microfinance practices can be seen as a continuation of pre-existing exploitative financial markets. These unregulated practices have been widely studied for their criminal use and negative impact on poverty, legitimizing pre-existing exploitative practices and allowing them to proliferate to the detriment of vulnerable sections of society.

Loan sharks are known for their predatory tactics, including charging exorbitant interest rates and employing coercive collection methods, which further trap borrowers in cycles of debt. The hype surrounding microfinance in the last few decades has, in some cases, masked these exploitative practices, enabling their persistence and growth.

To combat the insidious impact of “black” microfinance, it is imperative to raise awareness and advocate for greater transparency and accountability within the microfinance sector. Genuine microfinance institutions must uphold ethical lending practices, prioritize client protection, and promote financial literacy to empower borrowers and ensure their long-term financial stability.

“White” microfinance institutions operate under a business model focused on sustainable growth and poverty alleviation. These institutions prioritize responsible lending practices aimed at fostering entrepreneurship and productive economic activities within underserved communities. Studies indicate that responsible microfinance can lead to significant improvements in income and well-being among the poor. The success of Grameen Bank, the Bangladeshi microcredit organization, and other similar institutions demonstrates the potential positive impacts of well-managed microfinance programs on poverty alleviation.

The distinction between “black” and “white” microfinance lies not only in their approaches to financial service provision but also in their underlying impact on communities. While “white” microfinance embodies the principles of empowerment and social impact, “black” microfinance perpetuates cycles of poverty and exploitation. By shedding light on the darker shades of microfinance and advocating for ethical practices, we can strive towards a future where financial inclusion truly leads to prosperity for all. Drawing on existing research, this article underscores the necessity of transparency, accountability, and ethical practices in the microfinance sector.