Does microfinance deserve its bad reputation? It is certainly not without its challenges. However, evidence suggests that microfinance still has plenty to offer for poorer households.

Microfinance often gets a bad rap. A part of this stems from unrealistic expectations among donors, press and its most influential proponent, Nobel Prize winner Muhammad Yunus, that it could lift millions out of poverty.

In addition, a series of influential studies in development economics that used controlled field experiments failed to find evidence of large income and investment gains among recipients of microcredit.

Many people also have valid concerns about the welfare of borrowers. As microfinance has become more commercialized, with more privately owned providers, lenders have confronted poor borrowers with high interest rates and multiple micro-loans. Sometimes they have coerced borrowers into paying off those loans with higher interest rates.

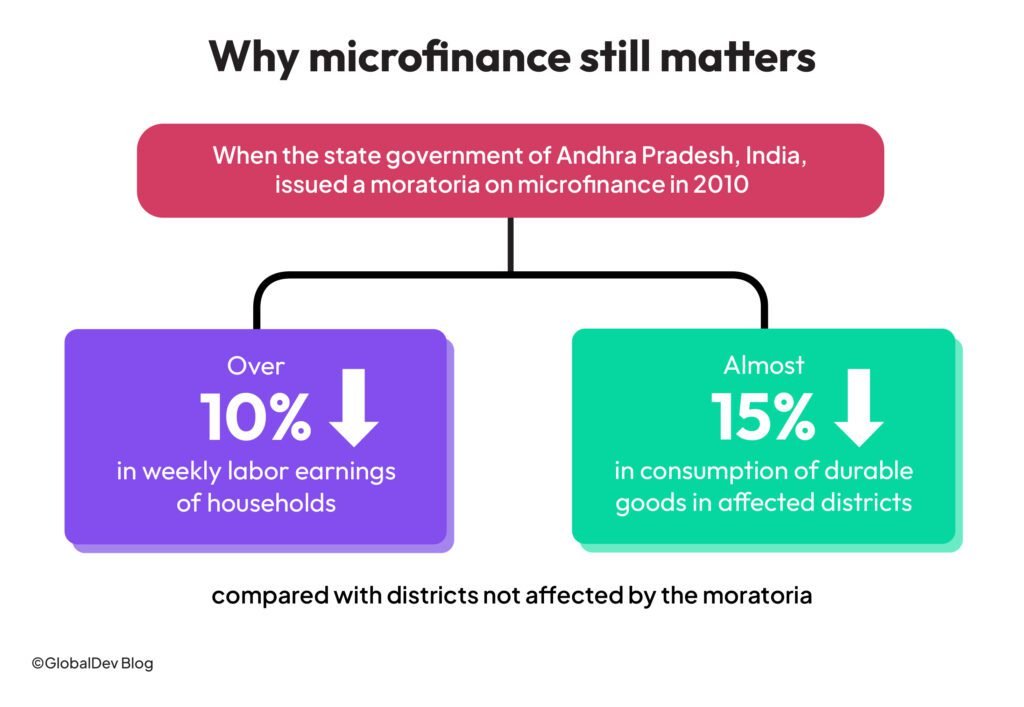

Yet, microfinance (particularly microcredit) is one of the most pervasive financial inclusion tools among the world’s poor. Not only do borrowers come back to their providers again and again, evidence shows that a loss of microfinance can affect earnings. For example, recent work shows that household incomes and financial inclusion suffered during moratoria on microlending in India.

In districts exposed to the moratoria in the state of Andhra Pradesh, the weekly labor earnings of households declined by over 10%, compared to households in districts that were not exposed. Furthermore, consumption of durable goods in affected districts declined by almost 15%.

Why people use microfinance

We are proud to have edited a new handbook that resolves this seeming contradiction and offers insight on how to deepen financial inclusion – a policy goal emphasized by many governments. The Handbook of Microfinance, Financial Inclusion and Development explains whom microfinance reaches, how it helps, and why clients come back.

As the Handbook shows, a part of the story is our lack of understanding as to why people want microfinance. Nor do we know why they return to it despite its risks and supposed lack of benefits. This is because many of us – including researchers, development practitioners, the press, and government officials – don’t think about how poor households live from day-to-day. This means we don’t measure poverty or deprivation well.

The fact is that people slip in and out of poverty, often within the same year. Jonathan Morduch shows in Chapter 2 of the Handbook that poverty is not just about a lack of money. Life in poverty is an interaction of insufficiency (a lack of money), instability (a lack of predictability about when money arrives), and illiquidity (a lack of enough money on hand to meet immediate, often unexpected, needs).

Tools like microcredit, savings, and insurance can be vital to the poor in reducing instability and short-term illiquidity, even if they don’t make a large difference to annual incomes in all contexts.

How microfinance has been studied influences perceptions

The benefits of microfinance and financial inclusion are also under-appreciated, in part, because of how economists have studied them. Begonia Gutiérrez-Nieto and Carlos Serrano-Cinca in Chapter 3 of the Handbook argue that early qualitative research on microfinance outreach and social outcomes exaggerated expectations for microfinance. These qualitative methods gradually gave way to more quantitative studies, including those that use rigorous randomized controlled trials (RCTs).

But these quantitative methods made it harder to see the full range of benefits from microfinance, because they are inherently difficult to identify. In the case of RCTs, benefits are difficult to generalize because they are highly specific to the local context in which microfinance occurs and to the provider.

In contrast, financial diaries, which track all financial inflows and outflows of poor households, and the aforementioned studies of sudden stops to microfinance provision (as in India), provide a richer picture of how microfinance is used and its overall impact on poor households.

Fairness and reaching women and the rural poor

Concerns about the fairness of microfinance and over-indebtedness are valid. The Handbook addresses these head-on. It shows that it is possible to keep interest rates low by targeting diverse borrowers and through innovative measures that make microfinance programs more efficient.

Meanwhile, products that incorporate local cultural gender norms can avoid over-indebtedness and empower women borrowers. In rural areas, finance that enables poor farmers to participate in agricultural value chains and agricultural insurance products for smallholder producers can improve financial inclusion.

Traditional and new delivery channels play important roles

There are good reasons to expect microfinance to keep playing an important and beneficial role for the poor. Traditional delivery channels, such as group liability lending, will continue to rely on local information about the creditworthiness of borrowers to provide credit in places where formal banks can or will not.

And new delivery channels for financial services – such as agent networks, due to their close physical and social proximity to poor borrowers – and digital finance, hold great promise for reducing costs and improving convenience and security for poor people and under-served communities. They can also help foster financial resilience in emergencies.

For poor households to reap the most benefits from new financial products and delivery channels requires experience with financial services. This is sorely lacking in many pockets of the world, especially among the poor. Financial education can play an important role in all of this, and new approaches such as ‘edutainment’ via television programs and inclusion of financial education in high school curricula show promise.

However, as inexperienced users are drawn into financial services, effective consumer protection becomes increasingly crucial. Methods to protect the personal data of users from misuse are also critical.

Deeper and more meaningful financial inclusion

Microfinance is no longer the flavor of the month in development, far from it. But if we can overcome its challenges, it holds the promise of deeper and more meaningful financial inclusion for poor households.

Through microfinance branches and agents, the infrastructure is already in place to reach millions of clients. It is a matter of better adapting products and processes to meet the needs of poor clients. While some don’t see a rosy future for microfinance, the Handbook provides evidence that rumors of its demise are greatly exaggerated.