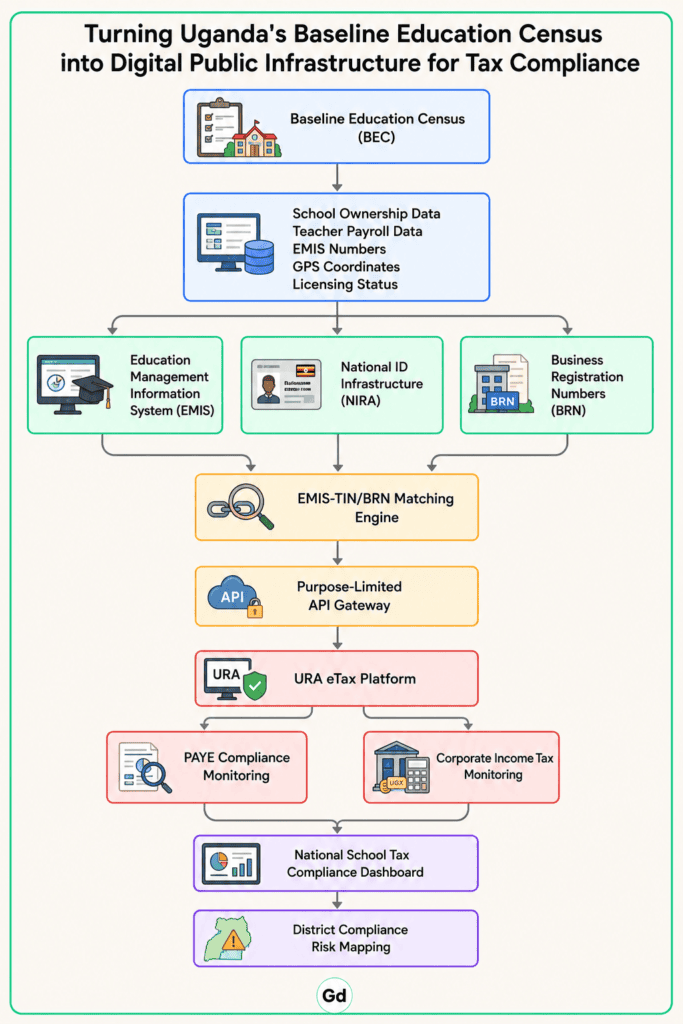

Uganda’s maiden Baseline Education Census maps more than 100,000 schools and institutions, recording ownership structures, teacher payrolls, and GPS coordinates for every registered school in the country. Connecting this data to Uganda’s tax system could substantially broaden the revenue base, with the numbers to make that case now traceable and defensible for the first time.

The central promise of Digital Public Infrastructure (DPI) is to make existing governmental systems speak to each other more effectively. That is a vision about state capacity as much as it is about technology. In the context of fiscal policy, the idea is that governments already hold the data they need to broaden the revenue base, and that what is missing is not information but connectivity.

Nowhere is this more tangible in Uganda today than in the relationship between education data and tax compliance. In May 2026, the Uganda Bureau of Statistics disseminated the maiden Baseline Education Census, mapping the country’s private pre-primary and primary schools, recording ownership structures, teacher payrolls, GPS coordinates, and licensing status.

For the first time, Uganda has a dataset containing precisely the information the Uganda Revenue Authority (URA) needs to identify which private schools are not paying their taxes.

Building the dataset

Uganda already holds three foundational building blocks for effective DPI in this context. The National Identification and Registration Authority administers the national identity register. The Ministry of Education and Sports maintains the Education Management Information System. URA operates the eTax platform. The census is the connective tissue: comprehensive, independently verified, and complete with ownership classifications, teacher headcounts, and school identifiers that can anchor tax compliance matching across all three entities.

What makes the census fiscally significant is its contents as much as its scale. For every institution, enumerators recorded ownership type, whether a sole proprietorship, limited company, religious body, or non-governmental organization: the same categories URA applies when assessing business income tax.

The EMIS number, mandatory for all registered schools, functions as a unique identifier matchable against the taxpayer registry. Tax Identification Numbers were also collected on a voluntary basis, meaning many private schools disclosed their tax identity in an official dataset for the first time.

Schools were geo-tagged, enabling mapped compliance monitoring, and the Uganda Bureau of Statistics (UBOS) has built a live interactive data portal where authorized agencies can query all of this by region, ownership type, and registration status.

The revenue potential is now calculable rather than speculative, though the figures that follow are estimates drawn from publicly available data and should not be read as official URA projections.

Transforming the tax base

A government program supporting teachers in private schools shows that there are approximately 150,000 people on private school payrolls in Uganda. At a conservative average salary of 300,000 Uganda shillings (about US$80) per month, the income tax potential from this workforce at a 10% effective rate is approximately 54 billion Ugandan shillings per year (about US$14.3 million). Even if only two-thirds of these workers are ultimately brought into compliance, the figure settles at around 36 billion Ugandan shillings (US$10 million) – roughly comparable in scale to Uganda’s annual per-pupil primary school subsidy.

The corporate tax picture is equally tractable. Schools registered as companies pay income tax on taxable profits at 30% under the Income Tax Act. Assuming there are 1,000 company-registered schools each earning 50 million Ugandan shillings (US$13,000) in taxable profit, the total annual exposure reaches 15 billion Ugandan shillings (US$4 million). At an average taxable profit of 20 million Ugandan shillings (US$5,300) per company-registered school, it falls to 6 billion Ugandan shillings (US$1.6 million).

The precise figure can only be established by testing declared profits against actual records, and that exercise first requires knowing which schools are companies. The census now provides that foundation.

Deploying the new dataset

The integration architecture follows four practical steps. A joint taskforce from URA, the Ministry of Education, and UBOS would match every EMIS number against the taxpayer registry, flagging schools with no corresponding tax identity. Business Registration Numbers, now being merged with TINs under the Tax Procedures Code Act, would become mandatory for school licensing renewal. A secure, purpose-limited API would connect EMIS to the eTax platform, synchronizing ownership changes, payroll figures, and operational status in near real time. URA would then create a compliance dashboard displaying PAYE and corporate tax filing status for each school by district.

None of this requires building anything new. In fact, Uganda is already moving in this direction. Under the Tax Procedures Code Act introduced last July, the government mandated replacing TINs with National Identification Numbers for individuals and Business Registration Numbers for entities. Linking EMIS to this unified identifier architecture is a logical extension to that reform, requiring coordination rather than new investment.

Even so, the risks must not be understated. Where school proprietors deliberately underreport enrollment to avoid tax scrutiny (as The Observer has documented), enforcement-first approaches risk driving the situation further underground.

Three safeguards grounded in Uganda’s Data Protection and Privacy Act 2019 are therefore essential. Purpose limitation means data shared from EMIS to URA is restricted by law to taxpayer identification and compliance risk assessment only. Data minimization means URA accesses only ownership type, EMIS number, the proprietor’s NIN or Business Registration Number, payroll headcount, and operational status—not learner records or demographic data. Phased implementation means registration support and voluntary compliance must precede enforcement, building institutional trust before testing.

What next for DPI deployment?

Uganda’s tax-to-GDP ratio stands at approximately 13.6%, below the 15% threshold widely associated with sustainable public finance and below Uganda’s National Development Plan IV (NDP IV) target of 16%. Clearly, there is work to be done and DPI drawing together Uganda’s education system and taxation records could help make up lost ground.

Crucially, closing the gap cannot come from intensifying pressure on those already registered. It requires bringing the informally adjacent economy into view. Uganda’s Baseline Education Census has now done exactly that for one of the country’s largest and most under-taxed sectors. The data is there, now the question is whether the institutions are ready to use it.

This article is part of a series produced in collaboration with the International Centre for Tax and Development at the Institute of Development Studies (IDS), UK, exploring the role of Digital Public Infrastructure (DPI) in strengthening state capacity and fostering development. We welcome contributions to this series.